Will AI Eat Software Alive?

Why the "Per-Seat" Playbook is a Liability and Where the Real Moats are Being Created

For fifteen years, we’ve lived by Marc Andreessen’s gospel that “software is eating the world.” But walk into any VC partner meeting today, and the conversation has taken a predator-becomes-prey twist: Is AI now eating software?

The software sector just underwent a brutal re-rating. The iShares Expanded Tech-Software Sector ETF (IGV) is down roughly 26% from its 2025 highs, with nearly $800 billion in market cap vaporized from its top ten holdings alone since the start of 2026.

The market isn’t just worried about a “growth slowdown.” It’s questioning the terminal value of the SaaS business model itself.

As someone who has spent over 10 years backing European founders from product-market fit to scale, I see this not as the death of software (actually thanks to AI more software is created, faster than ever before), but there are shifts in where value and defensibility are created and the implications on the workforce.

1. The Death of the “Per-Seat” Toll Booth

The most successful SaaS companies of the last decade were essentially high-margin toll booths. They charged for “seats.” But agentic AI (autonomous systems that execute workflows rather than just providing a UI) is shifting the paradigm and making those seats obsolete.

If an AI agent can do the work of five junior analysts, why would a CFO pay for five licenses?

The Squeeze: Legacy “price-per-seat” models are under existential pressure.

The Pivot: We are seeing a shift toward outcome-based pricing - e.g. charging per successfully completed task (e.g., a resolved customer ticket) rather than human log-ins.

Insight: New AI tools redefine workflows, as they bypass traditional interfaces. This increases efficiency but also reduces transparencies and introduces risks and security implication.

2. Moats: Data Gravity vs. “Vibe Coding”

There’s a lot of hype around “vibe coding” - the idea that anyone can prompt a full application into existence. While this is great for “one-shot” demos, it doesn’t create a defensible business.

The real winners will be the Systems of Record.

Data Gravity: Industry-specific platforms (Vertical Software) for life sciences or the public sector store critical, proprietary data that AI needs to be useful. This data context is hard to extract and even harder for an AI-native newcomer to replicate from scratch.

Vertical Focus: Horizontal tools (general CRM, general HR) are vulnerable. Deeply embedded, mission-critical vertical software is where the “moats” actually hold.

3. Speedboats vs. Aircraft Carriers

Goldman Sachs1 highlights a central tension: Can incumbents like Salesforce or Workday re-architect fast enough?

They have the distribution, yes. But they also have “dinosaur mindsets” and massive technical debt. For a startup, the opportunity isn’t to build a better interface; it’s to re-architect with LLM reasoning at the core.

Incumbents are “fast followers” layering AI on top of legacy systems. Startups are the speedboats that can build AI-native workflows that bypass traditional menus and hard-coded logic entirely.

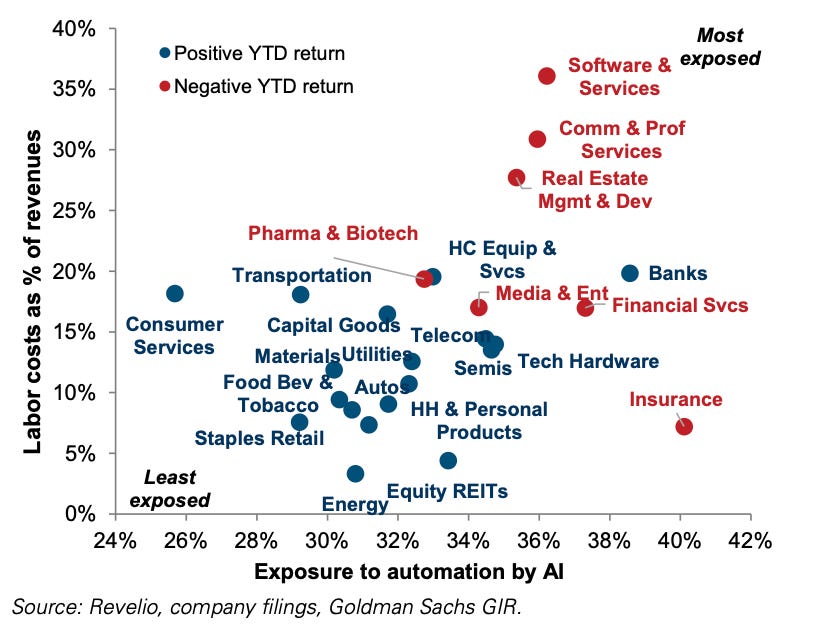

4. Investment Selectivity and Sector Impacts

We already see an extreme concentration of venture capital in a few companies, mostly AI ones. This is a consequence of the latest AI developments, impacting different sectors and business models differently.

Vulnerable Sectors: Digital advertising, gaming, and basic consumer-facing chatbots are highly exposed to disintermediation.

Promising Sectors: Infrastructure, Cybersecurity, and Data Management, which are viewed as catalysts for AI rather than victims of it.

5. Exit and Valuation Environment

While the current re-pricing on the stock-market might be an overreaction, similar to over-valuing AI companies. There are some fundamental considerations:

Valuation Compression: Higher uncertainty around the “terminal value” of software firms has led to sharp de-ratings. VC investors should be prepared for more conservative valuation multiples during follow-on rounds.

M&A Catalyst: Also the GoldmanSachs report suggests that incumbent firms may increasingly turn to M&A to acquire AI-native innovation they cannot build fast enough in-house.

Takeaway

To build a defensible business in the AI era, both founders and investors must look beyond the hype and grasp the structural shift in power. True defensibility comes from owning the System of Record, the proprietary data and industry context that AI needs to be useful but cannot easily replicate. Success requires maintaining strategic independence from the "infrastructure cartels" through healthy gross margins and a clear understanding of the limits of current models.

“The unimaginative investor asks: ‘Who does this AI replace?’ The visionary investor asks: ‘Who does this empower, and by how much?’”

I strongly believe that shifts in the computational fabric - the new possibilities of compute power available in data centers and at the edge - represent the single best opportunity in history to build category-defining companies. Now is the time to ride the tsunami.

Goldman Sachs report #146 from March 9th, 2026: https://www.goldmansachs.com/static-libs/pdf-redirect/prod/index.html?path=/pdfs/insights/goldman-sachs-research/will-ai-eat-software/report.pdf