The Survivability Compass

Why Most AI Companies Will Not Survive

After building and financing software companies for more than 20 years, from the SaaS era to today’s AI-native businesses, I have seen certain patterns repeat.

Markets become euphoric. Founders optimize for vanity metrics. Investors chase growth at any cost. And in the end, only a small number of companies capture nearly all long-term value. Don’t get me wrong, growth and efficient GTM are crucial, but they need to rest on a solid foundation.

When I look at the companies that endured versus those that disappeared, two dimensions consistently determine survivability:

Customer Love — how indispensable the product becomes.

Economic Quality — how efficiently the company delivers that value.

These two dimensions matter far more than headline growth.

1. Customer Love: Net Revenue Retention (NRR)

The strongest software companies are not merely useful, they become extremely difficult to replace.

Their defining characteristic is exceptional retention, usually expressed through Net Revenue Retention (NRR). NRR captures whether existing customers expand their spending over time. It is one of the clearest signals of product-market fit and customer dependency.

Importantly, strong NRR is often disconnected from short-term growth.

I have repeatedly seen companies with extraordinary NRR, sometimes above 140%, but only moderate growth because they lacked sales capacity or were undercapitalized. Those businesses are often vastly more valuable than high-growth companies with weak retention.

A company growing quickly with sub-100% NRR is effectively pouring water into a leaking bucket.

This is an external signal: it reflects how customers perceive and value the product.

2. Economic Quality: Gross Margin

The second variable is related to profitability. In software and high-growth technology businesses, I believe gross margin matters more than EBITDA in the early stages.

Why?

Because the entire venture-backed software model depends on building something once and distributing it repeatedly at near-zero incremental cost.

High gross margins create:

Greater reinvestment capacity

More pricing power

Faster product iteration

Stronger go-to-market leverage

Better resilience during downturns

For years, SaaS investors considered 80%+ gross margins world-class. But true outliers often operate above 90%. Those businesses can aggressively reinvest while still compounding efficiently.

Gross margin is therefore an internal signal: it reflects the company’s structural competitive advantage.

AI Changes the Cost Structure - Not the Principles

These principles remain true in the AI era.

What changed is infrastructure cost. Inference, token usage, and model compute introduced a new category of variable expense that many founders underestimate.

Today, many investors focus almost exclusively on revenue growth and ARR expansion. Few discuss churn or gross margin. The prevailing assumption is that scale alone will eventually solve the economics.

That assumption is dangerous.

I regularly see AI software companies operating at 60% gross margins because inference consumes 20% or more of revenue. Those are infrastructure-level margins — not software margins.

In contrast, the strongest AI companies often spend less than 10% of revenues on inference. Some already achieve 90%+ gross margins through:

Model optimization

Smaller task-specific architectures

Internal infrastructure ownership

Efficient inference routing

Fine-tuned compute utilization

These companies are structurally advantaged. In a future price war, they are best positioned to survive.

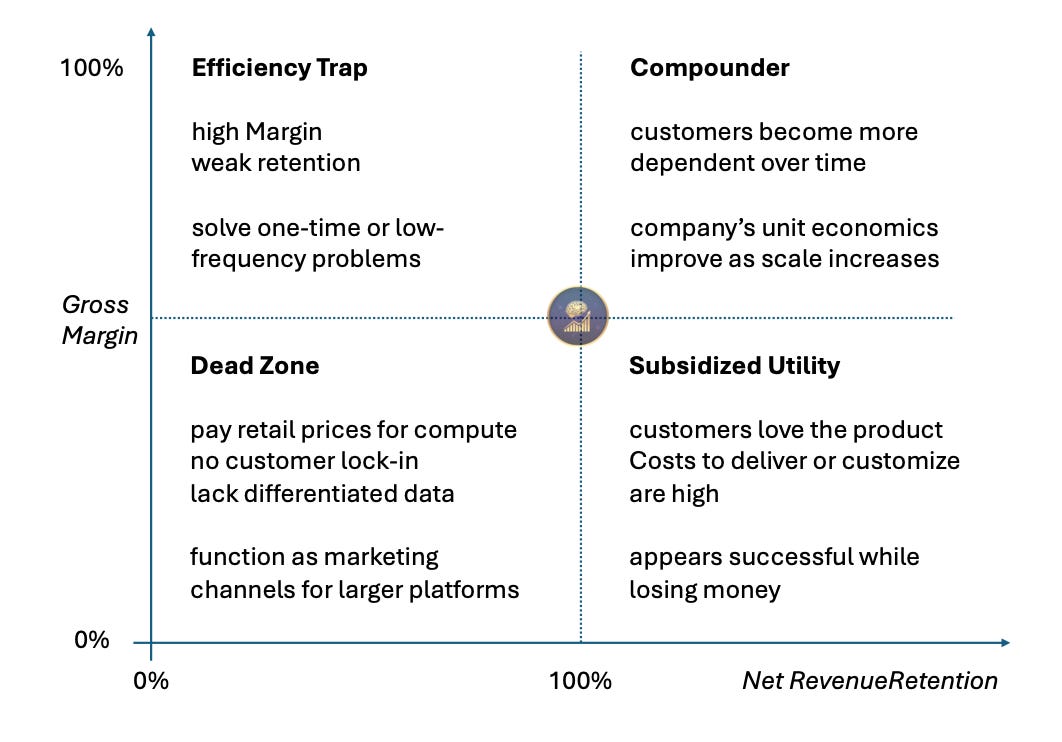

The Survivability Matrix

This led me to conceptualize the Survivability Matrix. The framework maps companies across two axes:

X-axis: Net Revenue Retention (0–>100%)

Y-axis: Gross Margin (0–100%)

Together, they reveal the survivability profile of a software or AI company. These axis form Four Quadrants

1. The Dead Zone (Bottom Left)

These companies are little more than interfaces layered on top of foundation models. They pay retail prices for compute, possess no customer lock-in, and lack differentiated data. In practice, they function as marketing channels for larger platforms.

2. The Efficiency Trap (Top Left)

These businesses look attractive on paper because margins are high. But retention is weak. Typically, they solve one-time or low-frequency problems. Eventually, customer acquisition costs exceed customer lifetime value.

3. The Subsidized Utility (Bottom Right)

This is common in enterprise AI. Customers love the product, but the startup spends enormous amounts on inference, services, or customization to deliver value. The business appears successful while quietly losing money on every customer. Without optimization or pricing power, the economics eventually collapse.

3. The Compounder (Top Right)

This is the target state. These companies combine:

High retention

High margins

Strong data gravity

Efficient infrastructure

Expanding workflows

Customers become increasingly dependent over time, while the company’s unit economics improve as scale increases. This is where enduring software companies are built.

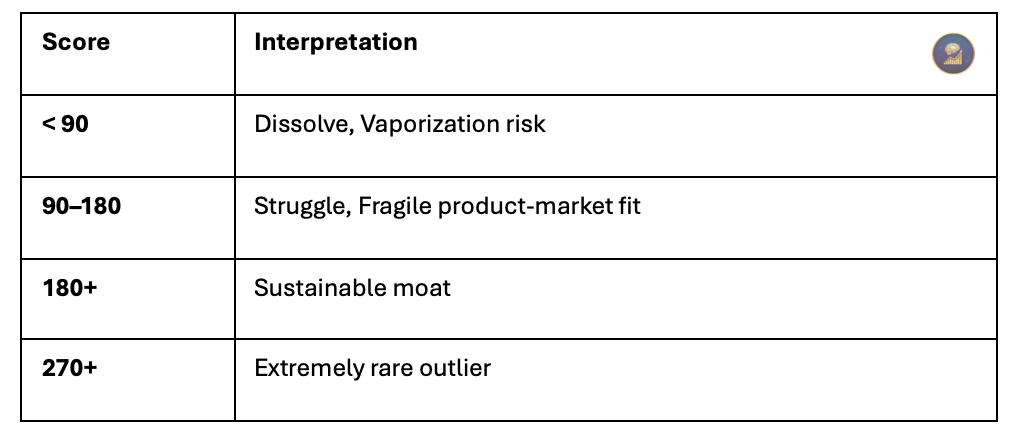

The Rule of 180

One observation became increasingly clear:

· Looking at NRR or gross margin individually is informative.

· Looking at them together is powerful.

So I began combining them:

Survivability Score = NRR + Gross Margin

Examples:

100% NRR + 80% Gross Margin = 180

120% NRR + 75% Gross Margin = 195

90% NRR + 60% Gross Margin = 150

Over time, a pattern emerged.

180 appears to be the survival threshold.

A score above 180 suggests a business with both customer stickiness and economic strength. Below that threshold, survivability deteriorates quickly.

In degrees of a circle 180, represents a horizontal line. Below it survival becomes uncratain, above it compounding begins. Hence I mapped the Survivability Score to the Gradiants of a circle to create the Survavability Compass.

Survivability Thresholds

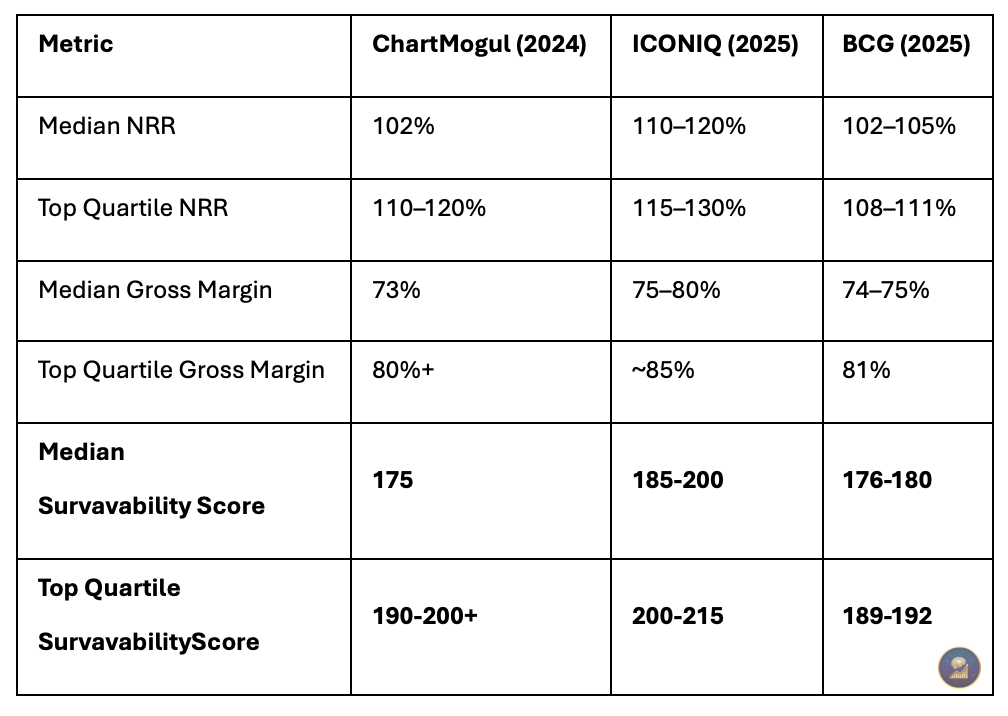

Benchmark Validation

I validated this concept with external benchmark data, which supports this framework.

Notably:

Median NRR plus median gross margin clusters around 180.

Vertical software businesses generally outperform horizontal software on both retention and margin.

Usage-based pricing consistently produces higher NRR than flat subscription models.

ICONIQ data, for example, shows usage-based pricing achieving roughly 135% NRR for sub-$100M ARR companies, versus approximately 121% for traditional subscription models.

The Historical Ceiling

Before AI, the highest NRR businesses were already showing the same dynamics.

Snowflake

Snowflake reached 158–171% NRR during its peak expansion years.

Without adding a single new customer, revenue from existing accounts increased dramatically as customers expanded storage and compute usage.

Datadog

Datadog sustained 130–140% NRR through successful land-and-expand execution.

Customers began with infrastructure monitoring and gradually adopted logging, security, and observability products.

The AI Infrastructure Winners

Today, the strongest AI infrastructure companies occupy the top-right quadrant.

Databricks

Databricks benefits from owning both the enterprise data layer and AI training workflows.

As customers train increasingly sophisticated private models, spend naturally expands.

Microsoft Azure AI

Azure benefits from enterprise-scale AI deployment.

A small OpenAI pilot can evolve into organization-wide infrastructure usage, dramatically increasing cloud spend over time.

The AI-Native Breakouts

Several AI-native companies are already showing elite survivability characteristics.

Harvey

Once integrated into legal workflows, usage expands naturally across teams and matters.

Cursor

Developers who adopt AI-native coding environments rarely revert to traditional workflows.

Expansion comes from team-wide deployment and increasingly autonomous AI-assisted development.

The Nvidia Anomaly (The 300° Club)

We have not talked about the fourth quadrant, the fabled one. Is it even possible to achieve a Survivability score of over 270? And I have to say there might be one outlier and that might be the reason this company is the most valuable company in the world: Nvidia. Combine Gross Margins of 75-78% with a revenue growth that is way above 200%. With customers begging to spend 3x more than the previous year, this

If we look at Nvidia in the current cycle:

Gross Margin: ~75% - 78%

Revenue Growth: (Which acts as a proxy for NRR when customers are doubling their chip orders every quarter)

When your customers are literally begging to spend 3x more with you this year than they did last year, your “Sustainability Score” breaks the circle.

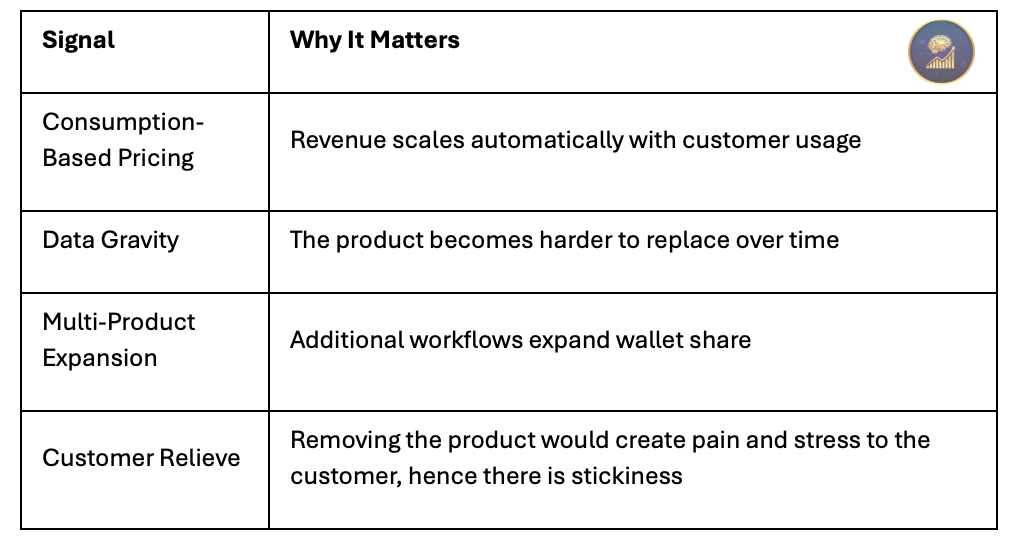

The Three Signals of Elite NRR

When evaluating whether a company can achieve truly exceptional retention, I look for three characteristics.

Final Thought

The software industry spent the last decade optimizing for growth. The AI era will reward survivability. The winners will not necessarily be the fastest-growing companies. They will be the companies that combine:

High customer dependency

Strong economic efficiency

Durable retention

Structural cost advantages

In the end, survivability compounds. Everything else fades.