💡 The Pitch Deck Paradox

Why Your Checklist Is Killing Your Narrative

We all know the essentials of a Series A pitch deck. As investors, we frequently share the expected table of contents, confirming it’s the “long form business card” necessary to convey interest. Founders, you meticulously cover the mandatory slides: Company purpose, Problem, Solution, Team, Market, and Traction. You invest in design, keep it brief (ideally under 15 slides), and ensure traction is front and center.

But this ritual compliance with the checklist highlights a critical, often fatal, misunderstanding: the list of topics is merely the raw material, not the structural logic.

The single most consequential red flag we encounter is the “Poor storyline”. This isn’t a failure to write well; it is a fundamental failure of linear thinking. By delivering a sequence of facts without an explicit, compelling logical argument, you force the investor to manufacture the narrative themselves.

This inevitably strains the reader’s mental energy, leading to misinterpretation, confusion, and ultimately, a ‘pass’. The problem isn’t the data you have, it’s the sequence in which you present it.

The Fix: Mastering the Logic of the Argument

The antidote to the “poor storyline” is deploying the Pyramid Principle as your core communication strategy, ensuring your entire deck forms a structure that works downward from a single, compelling thesis.

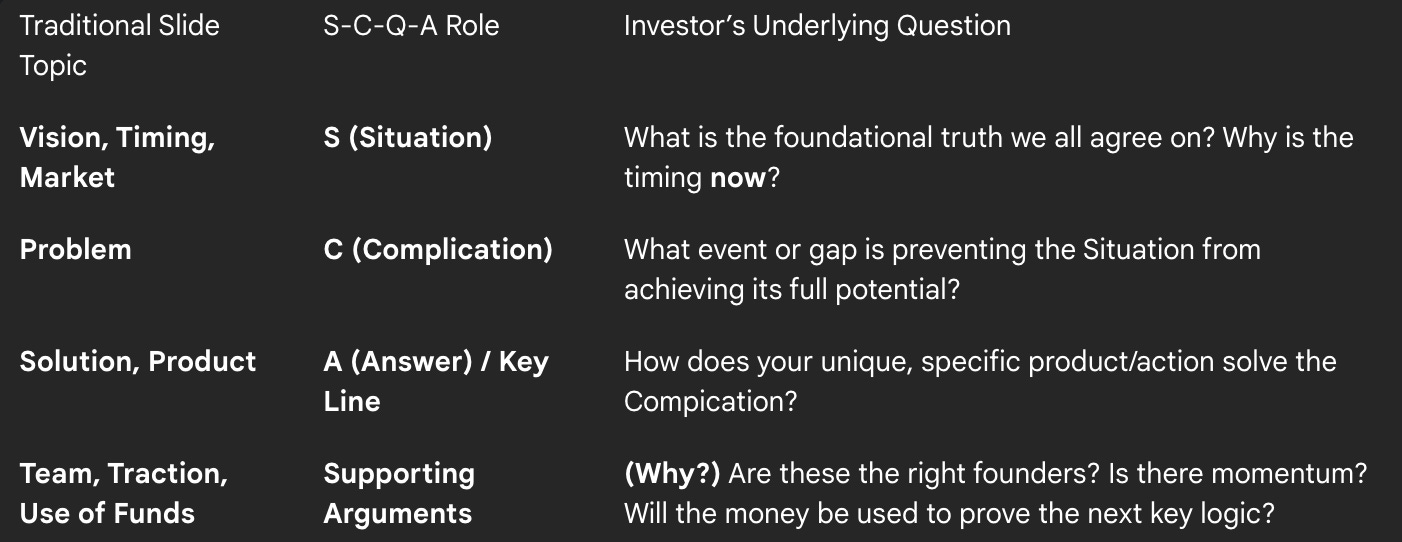

This structure operates on one universal logic for effective communication: Situation-Complication-Question-Answer (S-C-Q-A). Your entire deck must be built to answer a question the investor already has in their mind.

Your remaining slides—Traction, Team, Business Model, etc.—then become the Key Line supporting arguments, designed to answer the single, unavoidable question raised by the Answer: “Why?“ or “How?“.

The clearest sequence is always to give the summarizing idea before giving the individual ideas being summarized. If your solution slide starts with a feature list instead of the core value proposition, you’ve reversed the logic.

Decoding Red Flags: The Investor’s Thinking Check

The cautionary ‘red flags’ we observe are often indirect measurements of a founder’s conviction and intellectual maturity:

Poor Storyline: A direct failure of logical thinking. It betrays a core weakness in thinking through the cause-and-effect chain of the business opportunity.

External Advisors: Pitch decks “visibly prepared by external advisors” raise questions about the team’s ability to communicate their own unique insight and demonstrate intellectual ownership. If you can’t articulate the argument, we won’t buy the premise.

Financial Disconnects: A slide that promises a mere “5-10x return to an investor by selling the company in 5 years” indicates a fundamental lack of understanding of venture economics and a short-term perspective. We are looking for the exponential outcome only achievable by those in for the long game.

We need to see that you understand the relationship between all the complex ideas in your business model and that you can make them mutually exclusive and collectively exhaustive (MECE). The messy process of sorting facts and deriving insights (”thinking from the bottom up”) must result in a beautifully clear articulation (”presentation from the top down”).

Your deck is the primary evidence of your clarity of thought. Get the logic right, and the content problems disappear.

The Strategic Imperative

The time spent obsessing over the list of materials—from the financial model to the cap table and KPIs—is worthwhile only once the fundamental logical structure is sound. Investors demand evidence that the team possesses the Hard-Headed Thinking required to synthesize information and drive decisions.

You must internalize this truth: You must first perform the thinking from the bottom up, but you must always present the argument from the top down. If your entire thinking is not clear to the reader in the first 30 seconds of reading, you must rewrite.

What single statement, placed at the top of your deck, answers the biggest question in your market so inevitably that the investor has no choice but to ask, “Why do I not already own this?“