The Architecture of Alignment

Alpha isn’t found; it’s forged. A great deal doesn't fall from the tree - it is carefully crafted and negotiated into existence.

In the hyper-fueled echo chambers of Silicon Valley and the burgeoning tech hubs of Europe, we often treat fundraising like a finish line. We celebrate the “closing” as if the capital itself is the victory. However:

Deals do not simply “fall from trees” or appear as fully formed gifts from the market. They are surgical constructions. Mastering a deal is only partly about negotiation; it is foremost about alignment.

The Fertilizer Fallacy

Capital is a fertilizer: applied to a healthy, proven business model, it supercharges growth. Applied to the wrong team or at the wrong stage, it can act as a toxin, accelerating rot and ensuring a more public, more painful failure.

The craft of deal-structuring is the art of striking a balance that allows every stakeholder - founders, employees, and investors - to reinforce success while limiting the fallout of misalignment.

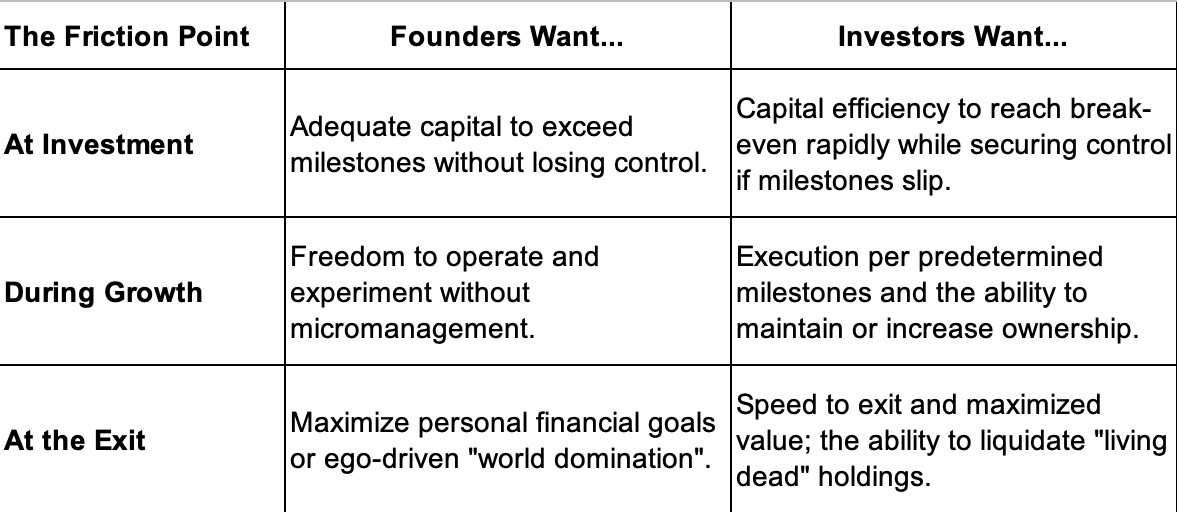

The Alignment Matrix: Managing the Friction

Every negotiation is a map of competing interests. To craft a deal that lasts a decade, requires stakeholder that can align where others fail.

The Structural Tools of the Craft

If alignment is the goal, term sheet clauses are the legal tools used to resolve the friction. You can divide these into two buckets: Economics (who gets the money) and Governance (who makes the decisions).

Liquidation Preferences as Floor Mats: These are not just “exit rules”; they are financial guarantees for when valuations fall. A savvy practitioner knows a lower valuation with “clean” 1x Non-Participating terms is often superior to a high “vanity” valuation encumbered by aggressive participating preferences.

Control Rights as Structural Walls: Investors install veto rights over asset sales, debt, and C-level hiring not to “run” the company, but to prevent “founder erraticism” and keep the entity on the rails.

Vesting as a Stability Mechanism: VCs don’t invest in code; they invest in the team’s ability to execute. Standard 4-year vesting with a 1-year cliff ensures that the equity “earned” reflects the time contributed to the company’s actual value.

The Internal Audit of Alignment

Before you enter a deal you should probe the ego of the founding team with brutal honesty:

Missionaries vs. Mercenaries: Are all founders in for the long haul, or will they act opportunistically on a quick exit that misses your return profile?

The Control Threshold: Are the founders truly aware that every dollar of outside capital is a share of future autonomy?

The Buffer Fallacy: Is this capital required to fill-in for holes, or is there a specific, aggressive use for every dollar?

The Bottom Line

A deal is not done until the cash is in the bank. But a good deal is one where the structure turns the team and investors into partners, rather than fellow sufferers on a preference stack.

Enduring companies are built by those who spend 100 hours achieving alignment before they spend an hour in negotiations or contract-drafting.

The full workshop and supporting materials are available for paid subscribers below: